Should your investment portfolio include commodities?

Oil, precious metals and agricultural crops are some of the commonly known commodities, which in turn are usually categorized as hard and soft. Gold, copper, aluminium, crude oil, natural gas and unleaded gasoline are referred to hard commodities since they require mining or drilling, whilst soft commodities are agricultural, such as corn, wheat, soybeans and livestock. Such raw materials depend heavily on supply and demand and are fundamental for the global economy. Developing countries for example, require heavy investment in commodities to build their infrastructure (steel and oil), to manufacture products (cotton and metals), and to proliferate food (agricultural crops) to sustain the increase in population.

Oil, precious metals and agricultural crops are some of the commonly known commodities, which in turn are usually categorized as hard and soft. Gold, copper, aluminium, crude oil, natural gas and unleaded gasoline are referred to hard commodities since they require mining or drilling, whilst soft commodities are agricultural, such as corn, wheat, soybeans and livestock. Such raw materials depend heavily on supply and demand and are fundamental for the global economy. Developing countries for example, require heavy investment in commodities to build their infrastructure (steel and oil), to manufacture products (cotton and metals), and to proliferate food (agricultural crops) to sustain the increase in population.

One can invest in commodities by actually acquiring the physical commodity and storing it. While this might be feasible for metal commodities and bars or coins, it gets more complicated in the case of oil, gas and corn. Another possibility would be to invest in future contracts or options. Futures are contracts to buy or sell commodities at a specified date and price in the future, including delivery. On the other hand, options on commodities futures give you the option not the obligation to buy or sell the futures at a stated price. Such products are complex instruments and are designed for companies within their respective commodity industry.

Diversely, investors may opt to buy shares of the companies that have a holding in the commodity such as oil and gas companies, or even precious metal streaming companies. In this circumstance, the share price doesn’t necessarily reflect the price of the commodity, as it also depends on various other company specific factors. Thus, the price of the share can plunge if the company does not deliver what investors would have projected. Most individual investors opt for exchange traded funds (ETFs) or mutual funds that correlate with commodities or commodity indexes to be able to get a wider exposure to a basket of commodities rather than exposing your portfolio to just one type of mineral within this sector.

The current market volatility is conveying real concerns about the economic impact of Covid-19, although this represents some interesting opportunities from which the commodities sector can benefit. Although most commodities and equity markets are uncorrelated, the commodities’ sector was hit badly with a decrease in demand for certain assets, such as crude oil and copper. As already highlighted above, various raw materials are essential for the global economy. One might ask, is it astute to invest in commodities when we are undergoing an economic slowdown?

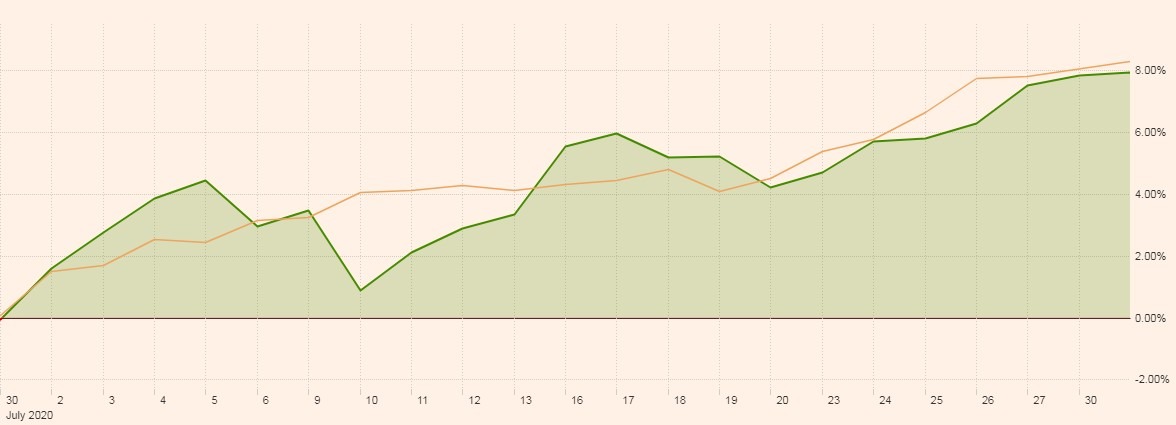

Throughout the month of August, commodities experienced their best month in over four years. This rally is illustrated in the chart below, which compares the performance of commodities against the S&P 500 index, which has hit its all-time high. For commodities, this monthly performance was also the second best performance in the past decade.

Bloomberg Commodity Total Return Index vs S&P 500 Index

*www.ft.com

Historically, commodities have a tendency to outperform other asset classes, especially equities, during times of unexpected high inflation. This was definitely the case in the mid-1970s and periods of the 1980s when inflation reached nearly 15%. While we don’t expect inflation to rise to those levels, investors’ inflation expectations have increased following the degree of fiscal stimulus and the US Federal Reserve’s (FED) aim to reach an average inflation rate of 2% over time to make up for past inflation target undershoots. This has partly contributed to the price increase in the last month since investing in commodities will hedge against inflation. Additionally, since most commodity prices are priced in US dollar, a weakening US dollar versus other major currency has supported commodity prices even further.

Governments and central banks have introduced various stimulus packages to boost their economies. The current low interest rate scenario is in fact one of the factors which is reducing the cost of borrowing and in turn reduce the cost of manufacturing and the cost of producing commodities. In August the FED pledged that monetary policy will remain accommodative. This should support demand for commodities and earnings for manufacturers.

From a demand perspective, due to urbanisation and a growing population, commodities remain supportive. The fact that governments are also investing more in their infrastructure to help boost economies, is another positive for commodities.

Commodities form part of the cyclical industries and depending on the market dynamics; different commodities tend to shift between being stable or volatile. Investors seeking long term growth should consider gaining some commodities’ exposure, as long as this falls within their risk tolerance and they are aware of what contributes to price fluctuations.

Matthew Magro, B.Com (Hons) Banking & Finance is an Investment Advisor at Jesmond Mizzi Financial Advisors Limited. This article does not intend to give investment advice and the contents therein should not be construed as such. The Company is licensed to conduct investment services by the MFSA and is a Member of the Malta Stock Exchange and a member of the Atlas Group. The directors or related parties, including the company, and their clients are likely to have an interest in securities mentioned in this article. Investors should remember that past performance is no guide to future performance and that the value of investments may go down as well as up. For further information contact Jesmond Mizzi Financial Advisors Limited of 67, Level 3, South Street, Valletta, on Tel: 2122 4410, or email [email protected]