High Yield Bonds Behaviour

Low interest rates and current economic conditions would lead us to rethink where is best to invest our hard earned savings. The term junk bonds have a tendency to scare people away with the idea that these are worthless investments. Nowadays these bonds are normally referred to as high yield bonds, some of which offer a good investment opportunity in investors’ portfolios. Just because these bonds have a lower rating than investment grade bonds, does not mean such bonds will fail. All market participants agree that these bonds are riskier than other bonds, yet they are less volatile than the stock market and, in their majority, high yield bonds end up generating higher returns than investment grade bonds. Thus, high yield bonds offer a balance between the stock market and the more stable investment grade bond market.

Low interest rates and current economic conditions would lead us to rethink where is best to invest our hard earned savings. The term junk bonds have a tendency to scare people away with the idea that these are worthless investments. Nowadays these bonds are normally referred to as high yield bonds, some of which offer a good investment opportunity in investors’ portfolios. Just because these bonds have a lower rating than investment grade bonds, does not mean such bonds will fail. All market participants agree that these bonds are riskier than other bonds, yet they are less volatile than the stock market and, in their majority, high yield bonds end up generating higher returns than investment grade bonds. Thus, high yield bonds offer a balance between the stock market and the more stable investment grade bond market.

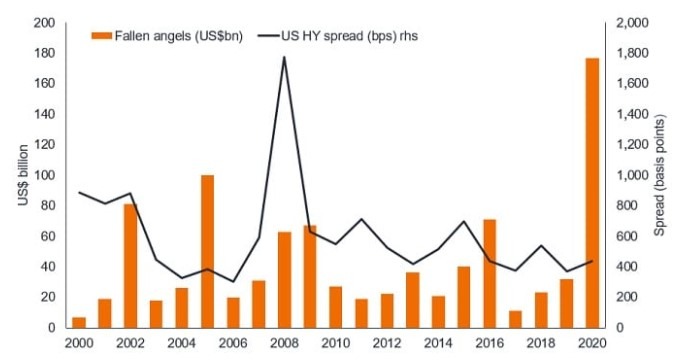

Last year was an exceptional year for bond downgrades from investment grade to non-investment grade where the high yield market has absorbed the supply that was created by the so called fallen angels. Such downgrades will increase the choice for high yield investors which was a rarity for the past few years, as can be illustrated in the chart below.

Fallen angels and US high Yield credit spread ending 2020

Source: J.P. Morgan, USD fallen angels in US$ billion at calendar year ends, 2020 as at 30 November 2020

Following these downgrades, the market strives to adopt the correct pricing of the bond which results in an opportunity to benefit from these price inefficiencies. This is expected to continue in 2021 although not at the same rate of the previous year. The fiscal and monetary stimulus approved by global central banks and governments early in 2020, gave a much-needed boost to demand for high yield bonds. In the near term such stimulus programs are expected to remain in force, hence allowing the high yield bond market to function better as demand and supply remain healthy.

These bonds are issued by companies that haven’t got an investment grade rating so they offer a higher return on investment. They pay a fixed interest rate which is normally distributed annually or half yearly as opposed to equities which pay a dividend depending on the company’s performance. These bonds carry a greater risk of default than investment grade bonds. However, if such companies default or go into liquidation, bondholders are ranked before shareholders so they stand a greater chance of receiving a percentage of the money invested. It’s important to keep in mind that certain companies that issue such bonds are reputable companies which would have seen their debt obligations explode due to the current economic scenario with the consequence of getting a rating downgrade.

Thus, research about the company or industry would help the financial analyst to understand whether the company is facing temporary or permanent financial difficulties. If the former prevails, the company would have the potential to improve with better economic conditions which in return will result in improving its credit rating whilst investors benefit from price appreciation. On the other hand, if the bond is downgraded further, the return on investment would reduce considerably. Another factor which might cause the price of these bonds to decrease is the perception that interest rates will start increasing. Although this would affect all types of bonds, high yield bonds stand a greater chance to fluctuate more due to the higher risk they contain. As a result, investors are hesitant to invest in these bonds which might cause liquidity problems if one tends to sell the bond on the secondary market.

What is the bottom line? On one hand, high yield bonds are more volatile and provide a higher risk than investment grade bonds. However, such securities might offer an opportunity when analysed wisely and can result to be a rewarding ingredient in your portfolio. Various analysts are forecasting that this year moderate positive returns are expected from high yield bonds, even though yields are historically low.

Really and thoroughly, whether or not to get a portfolio allocation in high yield bonds depends on the investor’s risk profile and investment objective. These can be assessed with an investment advisor who in return would be able to guide you depending on the score achieved to identify the best investment strategy.

Matthew Magro, B.Com (Hons) Banking & Finance is an Investment Advisor at Jesmond Mizzi Financial Advisors Limited. This article does not intend to give investment advice and the contents therein should not be construed as such. The Company is licensed to conduct investment services by the MFSA and is a Member of the Malta Stock Exchange and a member of the Atlas Group. The directors or related parties, including the company, and their clients are likely to have an interest in securities mentioned in this article. Investors should remember that past performance is no guide to future performance and that the value of investments may go down as well as up. For further information contact Jesmond Mizzi Financial Advisors Limited of 67, Level 3, South Street, Valletta, on Tel: 2122 4410, or email [email protected]