The abstract economic and investment scenario

July kicked off on a very positive note, with US equity markets flirting with record highs, as European bond yields settled at fresh record lows, while those in the US also reaching lows not seen in years. Why was this so? In a nutshell, a combination of some good news that came out from last weekend’s G20 summit, some mixed economic data in the US and Europe, and markets’ assumption that central banks are to remain accommodative for the foreseeable future.

The latter was further substantiated on Wednesday, following Christine Lagarde’s nomination to take the helm at the European Central Bank (ECB) from outgoing president Mario Draghi. Markets cheered to this fact, and immediately assumed that IMF’s current chief will join the dovish team. In layman’s terms, markets are expecting that the low-yielding environment and economic stimulus backed by the current ECB head, Mario Draghi, will be extended once Lagarde’s takes over the reins.

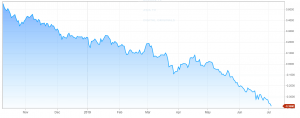

How did the bond market react?

As depicted below, the 10-year German Bund yield dipped further, to even reach a record low of negative 0.397% – a fraction shy from ECB’s minus 0.4% deposit rate. Such rate on the deposit facility, has remained unchanged at -0.4% since March 2016, and is essentially the rate banks may use to make overnight deposits with the Eurosystem. On the other hand, the -0.397% or so, on the 10-year German Bund is the gross yield to maturity should an investor decide to buy the German Government Bond maturing in 2029, retaining such an investment till that date, and reinvesting each and every coupon received through the term of the bond at the original yield to maturity. The point is that investors are ready not to earn money at all in the medium-to-long term on their cash held in a perceived safe-haven investment, on the back of a bleak economic scenario and anticipation for a continued accommodative monetary policy by the ECB.

10-year German Bund

In the US, Treasury yields have also witnessed a significant dip over the past few days, extending the dovish trajectory embarked upon since late 2018, which intensified on the turn of the year. In fact, the 10-year US Treasury yield earlier this week dropped to lows of 1.95% – last seen in November 2016, and substantially lower than the 3.2%+ yield at which it was trading just nine months ago.

What about total return performance for the different asset classes?

From an investment point of view, these past seven months served to be a win-win scenario for whoever held bonds as well as shares. Had one invested in the broader European Sovereign debt market since the beginning of 2019, on a total return basis, one would be in positive territory by some 7% at the time of writing. Meanwhile, Malta Government Stocks fared even better, with the MSE Malta Government Stocks Index up by over 8%. On the other hand, an investment portfolio consisting of more equities, such as the Euro Stoxx 600 index, would be up by nearly 20% – including reinvestment of dividends.

Gains were even more pronounced in the US, with the S&P 500 index hitting record highs on Wednesday, as bets on an interest rate cut occurring sooner rather than later lifted defensive sectors such as utilities, which are most sensitive to changes in interest rates. The equity index, by Wednesday’s session close, and ahead of the Independence Day holiday was up by 20.8% (including reinvestment of dividends).

On the other side, as treasury yields continued to slide further, the broader US sovereign debt market on a year-to-date basis is up by 5.5%.

What’s news and what’s not?

Although some form of optimism emerged from last weekend’s G20 summit, as trade tensions are expected to ease, the negative impact of the now more than a year-long trade dispute is materializing. Chinese people represent just under 19% of the world population and are crucial to global travelling. According to the United Nations’ World Tourism Organization, Chinese people also account to around a fifth of worldwide tourism spending. A surprisingly large figure considering the magnitude of such weighting and the repercussions it could have on the rest of the world.

Official data reported that Chinese people spent some 10% less outside their country in quarter one of 2019 when compared to the same quarter last year. Industry experts blame it on both a slowing economic environment together with a depreciating Chinese currency against the dollar. Over the past year, the yuan depreciated by some 3.5% against the dollar. As such, a Chinese traveller would be more inclined towards domestic travelling, at a cost of lost tourism to countries outside of China. US in particular registered close to 10% year-on-year decline, in Chinese visits in 2018, with further slowdown expected to have continued even throughout this year. This might eventually further impair the country with the longest economic expansion on record.

Despite of what has been an exceptional year so far in 2019 for financial markets, May apart, my concern predominantly revolves on its sustainability. Are markets perhaps assuming too much on what Central Banks can do to stimulate growth? What if the highly anticipated improved trade-relations and accommodative monetary stimulus (rate cuts) do not materialize? Whether a recessionary period will materialize anytime soon or not is rather subjective. What is for sure is that we ought to always be prepared for the unexpected, and always assess the performance of an investment portfolio or a particular asset class on a total return basis.

Colin Vella, CFA is Head of Wealth Management at Jesmond Mizzi Financial Advisors Limited. This article does not intend to give investment advice and the contents therein should not be construed as such. The Company is licensed to conduct investment services by the MFSA and is a Member of the Malta Stock Exchange and a member of the Atlas Group. The directors or related parties, including the company, and their clients are likely to have an interest in securities mentioned in this article. Investors should remember that past performance is no guide to future performance and that the value of investments may go down as well as up. For further information contact Jesmond Mizzi Financial Advisors Limited of 67, Level 3, South Street, Valletta, on Tel: 2122 4410, or email [email protected]